A bad life insurance plan is similar to a bad marriage.

We frequently join these coalitions with no idea of what to expect. Maybe we made a hurried choice or were given false hope by our loved ones or friends… Whatever the situation, you should be relieved that you are not alone.

Such remorse is not uncommon, especially when we know so little about life insurance policies.

But our goal is not to make you feel down. Instead, we want to let you know that the process of divorcing a life insurance policy is generally simple, rewarding, and not too messy.

So let’s get together to discuss how you can end this unpleasant relationship.

Recognizing the kind of life insurance policy you own

It’s crucial to know what kind of life insurance policy you have before we go through the step-by-step procedure for surrendering a life insurance policy. (That’s because the exit procedures for various policies vary.)

What we suggest.

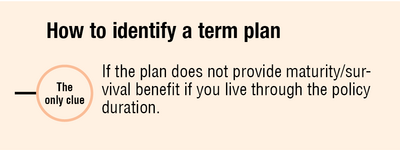

Term plans are the BEST of the three types of life insurance policies! Stick to your long-term plan if you have one.

However, be aware that certain term plans make the promise to reimburse the payment at the conclusion of the policy. Such programmes, nevertheless, are typically pricey and ought to be avoided.

However, whether you have a ULIP, endowment, classic, or money-back policy plan and want to quit your connection, follow these steps.

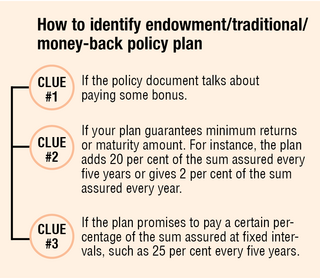

How to leave your ULIP will be the main topic of this post. For people who have an endowment, conventional, or money-back policy plan, please visit this website.

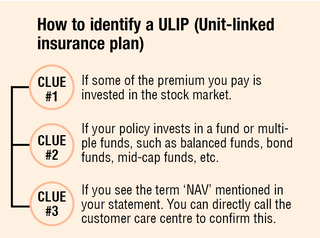

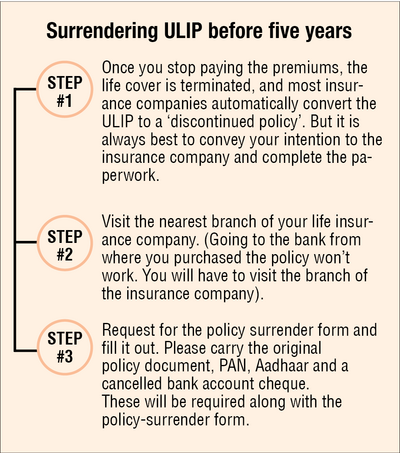

ULIP surrendering procedure

ULIPs have a five-year lock-in term that is required; no matter what, you may only withdraw the money you have already invested or paid as premiums once the five years have passed.

However, this does not obligate you to keep paying the premium for the whole five years. In reality, it is reversible at any time.

- Things to remember

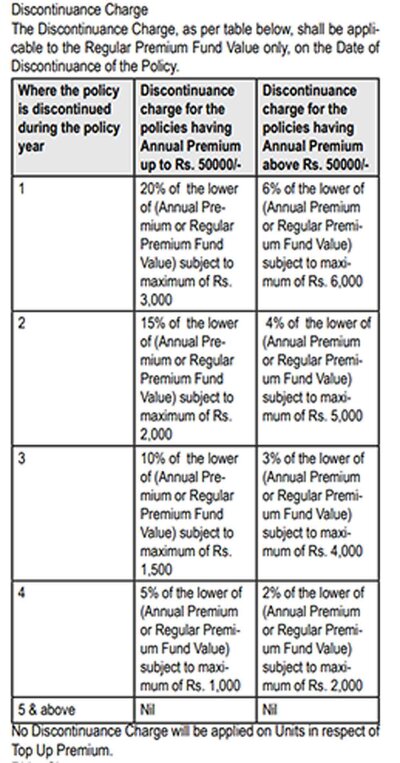

The insurance provider will deduct certain fees (discontinuance fees) from the investment’s market value.

From policy to policy, the quantity specified in the policy document varies. Typically, it is highest in the first five years. - The remaining funds are moved to a “discontinued policy fund,” where they continue to collect interest up until the lock-in period is up, at a rate of around 4% annually. The money is then deposited into your bank account.

- Insurance companies often continue to take a 0.50 percent fee during this time.

following the five-year lock-in period, giving up - The process is unchanged (as mentioned in the above process). The main difference is that the insurance company will pay you directly for the proceeds after deducting discontinuance expenses rather than putting your money to the “discontinued policy fund.”

Just as an illustration, here is how discontinuance fees for a ULIP from a leading insurance company in India appear.