Why More Indians Are Surrendering Their Life Insurance Policies

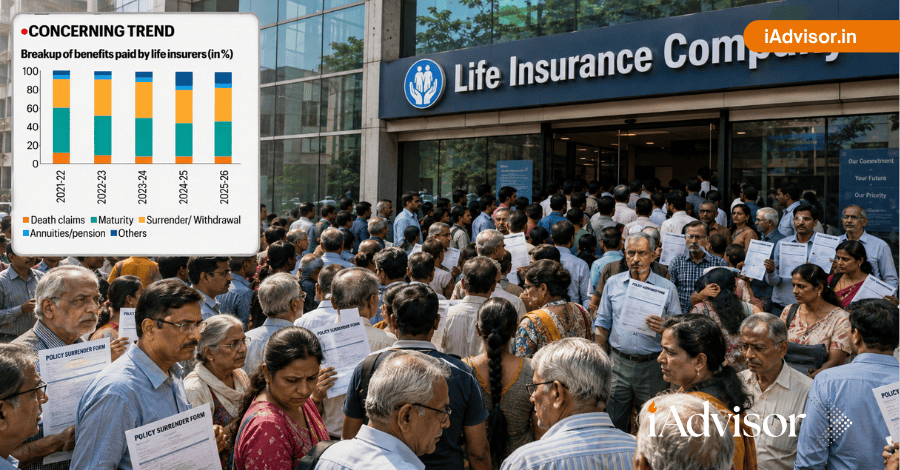

Every year the number of life insurance policy surrender cases are increasing in India. Recent industry data has revealed that surrender and withdrawal payouts have risen significantly, even when approaching the maturity dates in some cases. This shift has also attracted the attention of the Reserve Bank of India (RBI), which has highlighted the potential impact on insurers’ financial management.

If you are considering surrendering your existing life insurance policy, seek an independent review before making a final decision. A professional assessment may reveal better alternatives that preserve your insurance cover while helping you manage your financial situation.

Remember, the cost of losing life insurance protection can be much higher than the money received through an early surrender.

Why More Indians Are Surrendering Their Life Insurance Policies Read More »