Unit Linked Insurance Plan (ULIP) is a multi-faceted life insurance product. A ULIP is a life insurance and investment plan in one. As a policyholder, you must make regular premium payments, a portion of which is used to provide life insurance coverage. The remainder is combined with assets received from other policyholders and invested in financial instruments (equity and debt) in a manner similar to mutual funds. Investing in ULIPs allows you to be financially secure in the event of an emergency while also increasing the value of your money.

Let’s take a closer look at what a ULIP plan is and how to invest in one.

Benefits of a ULIP Plan You Should Know

Are you concerned about the advantages of a ULIP plan? A ULIP is a long-term investment option that allows you to invest in a variety of market-related instruments such as equities, debt, and balanced funds. Unit Linked Insurance Plans, or ULIPs, are mutual fund investments that are exposed to market swings. So, depending on your risk appetite and investing objectives, you can invest in a range of fund options with a ULIP plan.

You may also use a ULIP calculator to receive an idea of the premium you’ll have to pay and the predicted returns, which will help you better grasp what a ULIP plan is and the benefits it offers. Here are some other benefits of ULIP plans

1. Market Linked Returns

A ULIP is a type of insurance that allows you to earn market-linked returns by investing a portion of your premium in market-linked instruments like debt and equity (in varying proportions).

2. Savings and Life Insurance

Unit linked Insurance Plans (ULIP full form) help protect you and your loved ones against life’s unexpected events by allocating a portion of the premium to market-linked instruments.

As a result, you can benefit from market-linked returns while having your protection needs met by a ULIP plan.

With the need for protection against life’s unforeseen events taken care of, you can develop a regular saving and investing habit and accumulate substantial wealth over time with ULIP plans.

3. Flexibility

ULIPs, or Unit Linked Insurance Plans (ULIP full form), assist you in achieving your financial goals by allowing you to:

Depending on your changing needs, switch between investment funds.

After the initial 5-year lock-in period has ended, you can make partial withdrawals.

Single premium additions allow you to invest additional funds (in addition to the regular premium) as and when needed.

4. Level Paying Premiums

All regular premium or limited-term premium payments under a ULIP plan must follow a uniform or level premium payment structure. To provide life insurance coverage, any additional premium payments are treated as a single premium.

5. Charges Distributed Evenly

According to IRDAI, the charges levied on ULIP plans are evenly distributed over the 5-year lock-in period in order to help insurers avoid high upfront expenses. Before investing your money, make sure you understand the ULIP plan charges you’ll be paying.

6. Tax Benefits

The premiums paid for ULIP plans are tax-deductible up to a maximum of Rs. 1.5 lakh under Section 80C of the Income Tax Act of 1961. At the same time, the ULIP plan’s maturity/death benefit is tax-free under Section 10(10D) of the Income Tax Act 1961.

How to Choose the Best ULIP Plan?

Once you understand what the ULIP plan is, the next step is to choose the best-suited policy for you since there is a variety of options available. So, before you invest in a ULIP plan, you must consider comparing and evaluating to choose the best ULIP plan available in India. Following are some of the key points to keep in mind while choosing the best ULIP plan:

- Evaluate Your Goals

- Choose the Right Life Insurance Cover Amount

- Stay Invested for an Extended Investment Tenure

- Avail Maximum Tax Benefits u/s 80C & 10 (10D)

Max Life Insurance offers ULIP plans that are designed to meet the requirements of diverse financial profiles. Find out more about Max Life Online Savings Plan, Max Life Fast Track Super and more to start planning your future efficiently.

Which Investor Class Are ULIPs Most Suited For?

1. Individuals who want to track their investments closely

A ULIP plan allows you (as the policyholder) to closely monitor your portfolio. Such individuals may also benefit from the switching flexibility offered by ULIP plans, thorough which they can adjust capital allocation between funds options with varying risk-return profiles. ULIP means more control over your financial planning, including investment and insurance decisions.

2. Individuals with a Medium to Extended Investment Horizon

ULIP plan is ideal for you if you are willing to stay invested for relatively long periods.

3. Individuals with Varying Risk Profiles

ULIP plans offer a variety of funds options – each with varying risk-return profiles. Thus, investors with different risk profiles (from risk-averse investors to those with healthy risk appetite) must understand what is ULIP plan funds available before investing, so they can keep appropriate return expectations.

4. Investors across All Stages of Life

Different types of ULIP plans are available to help you protect yourself and your loved ones against financial needs and liabilities at specific points in time.

Fund Option Under ULIPs

Some of the most common investment options available under ULIP plans are –

a) Equity Funds

In an equity fund of ULIP plans, the allocated investment amount is used to purchase stocks, which have a Net Asset Value (or NAV) associated with them. NAV is the price per share (or ‘unit’) in a Fund. As the ULIP full form suggests, ULIP plan is a market-linked instrument, so the investments in equity carry high inherent risk because of market fluctuations. However, equity investments can also be the most rewarding.

b) Debt Funds

The premium allocated towards debt funds is used to invest in instruments such as Government Bonds, and debentures, which offer a lower risk than equity investments. Compared to equity investments in ULIP plans, however, debt funds may offer a lower return on investment.

c) Hybrid or Balanced Funds

Under ULIP plans, Hybrid or Balanced Funds are designed to provide capital growth (from the equity component) while ensuring lower risk (due to the debt component.) In case of market fluctuations, thus, any loss that you incur from the equity portion is balanced out by the lower risk yet consistent returns from the fund’s debt portion.

Understanding what is ULIP plan and your investment objectives carefully will allow you to make sound choices.

Below table enumerates the various aspects of the ULIP plan fund options –

| General Description | Nature of Investments | Risk Category |

| Equity Funds | Primary investments include company stocks that focus on capital appreciation | High |

| Debt Funds | Investments include government securities, corporate bonds, and other fixed-income instruments | Low |

| Balanced/Hybrid Funds | Investments combine equity component with fixed interest instruments | Medium |

What is ULIP Calculator?

Now that you know what is ULIP plan and how it works, it is crucial to make appropriate estimations of your investment. A ULIP Calculator can help you to compare and evaluate before buying a ULIP plan in India. A ULIP Calculator is a tool which assists in calculating the maturity amount on the basis of the expected future investment value and returns under the ULIP policy. To calculate your possible returns from ULIP plan, you just need to provide your details, investment amount (exclusive GST), payment frequency, premium payment term and investment period. The calculator will provide the returns and life insurance cover amount.

How Does ULIPs Work?

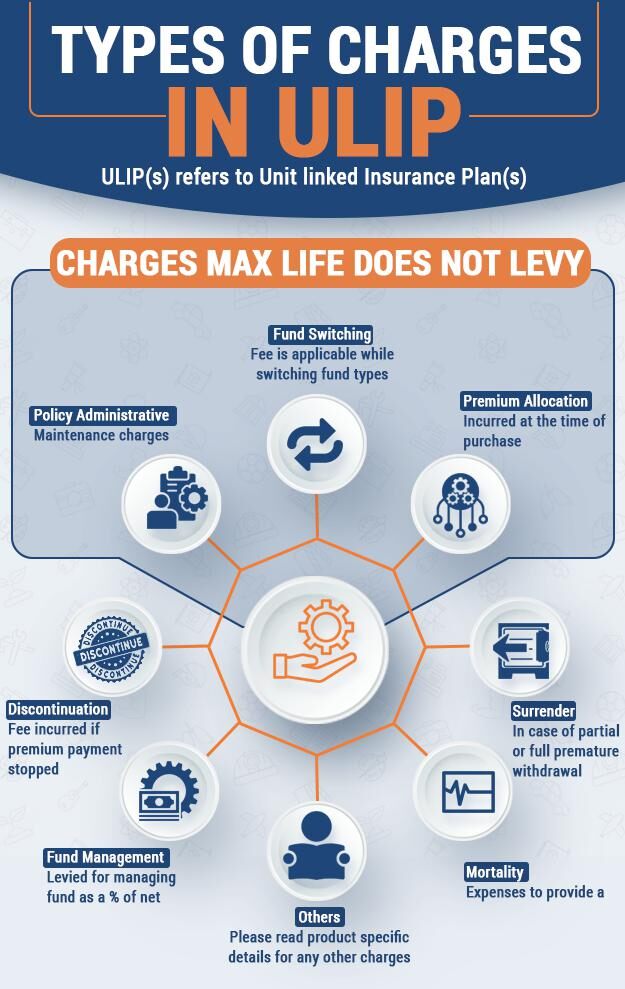

In a ULIP (ULIP full form – Unit Linked Insurance Plan), the premium amount that you pay is allocated to the funds chosen by you, after the insurance company has deducted certain charges, including –

1) Fund allocation charges

2) Policy administration charges

3) Fund management charges

4) Mortality Charges

As a long-term financial plan, ULIP means providing ample wealth creation opportunities. On the other hand, the ULIP’s meaning, as a life insurance product, is to provide more diversified returns in the form of life insurance protection.

The investments under ULIP plans are managed by dedicated fund managers, appointed by the insurance company. Thus, there is no need to track the investments on your own. If you want, you can track the performance of the individual ULIP plan fund options and switch between funds (without incurring any additional costs) to maximise the profit and deal with market volatility.

How Is ULIP Plan Structured?

The investment options under ULIP plan or Unit Linked Investment Plan are structured similar to those of mutual funds.

ULIP plans pool investments from different investors before they are allocated to different fund options based on individual preferences.

The assets under ULIP plans are managed by dedicated fund managers, whose focus is towards accomplishing specified investment objectives. As an investor, you can buy shares or ‘units’ in a single strategy or choose to diversify your investments across several market-linked ULIP funds.

When you choose to buy into a ULIP fund, you must first commit an initial lump sum payment. Subsequently, you have to make premium payments towards the plan – annual, semi-annual, or monthly. The premium payment obligation varies from one ULIP plan to another, as evident through the estimates made through the ULIP calculator. The premium invested in a ULIP plan is proportionally invested towards a specified investment mandate.

However, ULIP means flexibility to investors, allowing them to choose to adjust their fund preferences, depending upon their needs, throughout the investment duration.

Frequently Asked Questions (FAQs)

Q. What is ULIP and How does ULIP Plan Work?

A. ULIP full form is Unit Linked Insurance Plan, which is a type of life insurance solution, offered by insurance companies. These plans provide the combined benefits of life cover protection and investment returns.

ULIP plan provides capital market-linked returns on your investment, by allowing you to invest into a variety of equity and debt fund options.

Q. What should You Keep in Mind While Investing in ULIP?

A. While investing in ULIP plans, you must keep the following factors in mind –

- Applicable charges including surrender charges (those payable on premature surrender of ULIP plan)

- Investment fund options available

- Features and benefits

- Limitations and exclusions

- Consequences of ULIP plan lapsing

- Other disclosures

Q. How much of the premium paid is used to purchase units?

A. The entire amount invested under a ULIP plan is not allocated towards buying units. Instead, the insurance company allows the purchase of units only on the portion of the premium remaining once they have deducted the different fees and charges. The quantum of the capital amount received as premium and used to purchase units varies from one ULIP to another.

Overall, ULIP means that the cumulative monetary value of all the units purchased is invariably less than the total amount of premium received, because a portion of the capital is also allocated towards the life insurance coverage component.

Q. Can I seek a refund of premiums if I’m not satisfied with the ULIP policy, after purchasing it?

A. As a policyholder, you can request a refund of the amount of premium paid within the free-look period, if you disagree with the policy’s terms and conditions. In general, there is a 15-day free-look period, which starts once you receive the policy document. On opting for free-look cancellation you will receive the fund value, including charges levied via cancellation of units. The cancellation of units is subject to deduction of expenses towards stamp duty, medical examination, and proportionate risk premium for the coverage period.

Q. What is ULIP plan NAV?

A. ULIP plan NAV (or Net Asset Value) is defined as the total value of the units holding, after deducting the value of its liabilities. In other words, NAV is calculated after deducting liabilities such as management fees, marketing expenses, and operating expenses.

Q. When should I invest in ULIPs?

Individuals with a long-term financial plan for wealth growth and insurance should consider ULIP plans. However, there is no single right age to invest in ULIP. ULIP means you can grow your money and keep your family secure against emergencies so, whether you are planning for retirement, children’s education, and other financial goals, it can be beneficial.

Q. What can help me in maximizing my ULIP returns?

If you understand what is ULIP plan, you are aware of the market-linked return generations, therefore maximizing the returns depend on you risk-appetite and investment goals as an investor. Largely, you can keep a track of the market fluctuations and switch funds accordingly to optimize the ULIP plan benefits.

Q. How to calculate fund value in ULIP?

The fund value of ULIP plan refers to the overall monetary value of the policyholder’s units. The fund value on a given day can be calculated by multiplying the net asset value of each unit on that day by the number of units held.

Q. What is lock in period in ULIP?

Unit-linked insurance plans have a five-year lock-in period, during which the plan holder is unable to withdraw or liquidate the fund’s assets. So, investing in ULIP means preparing for long-term financial goals.

Q. Will I have to pay tax on ULIP maturity amount?

As per the Budget 2021, ULIP plans with annual premiums exceeding Rs 2.5 lakh are not eligible for tax-free maturity proceeds.