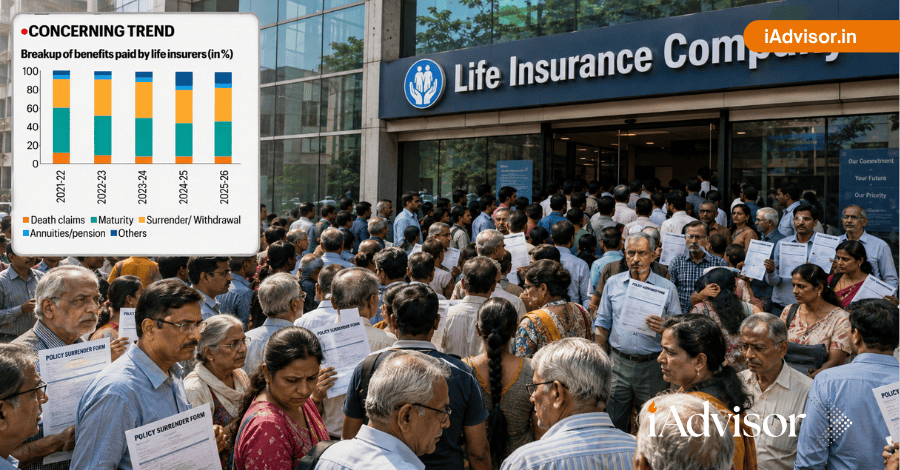

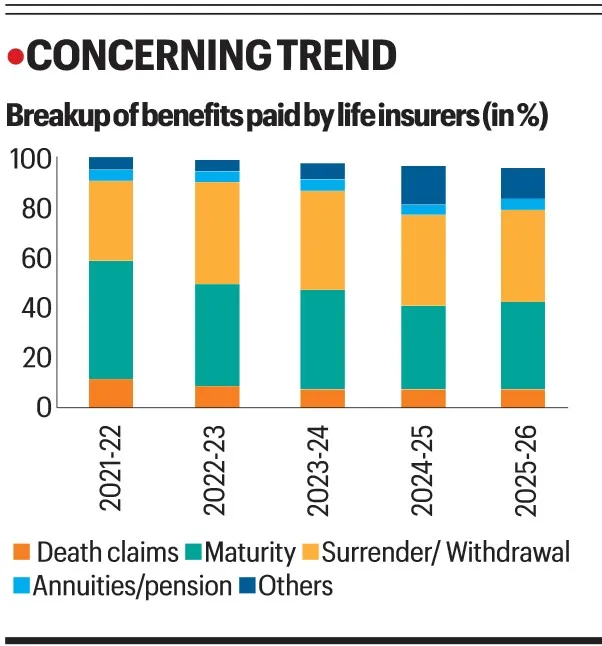

An increasing number of policyholders in India are surrendering their life insurance policies before maturity. Recent industry data has revealed that surrender and withdrawal payouts have risen significantly, even approaching the value of maturity payouts in some cases. This shift has also attracted the attention of the Reserve Bank of India (RBI), which has highlighted the potential impact on insurers’ financial management.

While surrendering a life insurance policy may seem like an easy solution during financial hardship, it often results in substantial financial losses and leaves families without adequate protection. Understanding why this trend is increasing can help policyholders make informed decisions.

Why Are More Indians Surrendering Their Life Insurance Policies?

There isn’t a single reason behind the growing number of policy surrenders. Instead, it is the result of several financial and behavioural factors.

1. Financial Pressure on Households

Rising inflation, increasing loan EMIs, higher education costs, unexpected medical expenses, and uncertain income have put pressure on household budgets. When families need immediate liquidity, life insurance policies often become one of the assets they consider cashing in.

However, surrendering a policy in its early years usually means receiving far less than the total premiums paid, making it an expensive source of emergency funds.

2. Mis-selling of Insurance Products

One of the biggest reasons for policy surrender is that many customers purchased insurance for the wrong reasons. Traditional life insurance plans are often marketed primarily as investment or tax-saving products instead of financial protection tools.

When policyholders later realise that returns are lower than expected or the product does not align with their financial goals and that they have been mis-sold to, they decide to surrender the policy.

In many cases, the problem lies not with insurance itself but with poor financial advice at the time of purchase.

3. Better Investment Awareness

Today’s investors have access to a wide range of investment options including mutual funds, ETFs, fixed deposits, bonds and retirement products. As financial literacy improves, many people compare the returns from traditional insurance policies with other investments.

While reviewing investments is a healthy financial habit, replacing insurance without arranging adequate life cover can expose a family to serious financial risks.

Why Is the RBI Concerned?

Life insurance companies invest premiums assuming that most policies will remain active for many years. When a large number of policyholders surrender early, insurers must arrange immediate funds to pay surrender benefits.

This creates additional pressure on their Asset-Liability Management (ALM), which refers to balancing long-term investments with short-term payment obligations.

The RBI has highlighted this growing trend because a sharp increase in surrender payouts could impact insurers’ liquidity planning and long-term financial management.

Does Surrendering a Policy Always Make Sense?

Not necessarily.

There are situations where surrendering a policy may be justified, such as:

- The policy was clearly mis-sold.

- The premium has become genuinely unaffordable.

- Your financial goals have changed significantly.

- You have already secured sufficient life insurance through another policy.

However, surrendering should never be the first option simply because the policy appears to offer lower returns than other investments.

Before taking such a decision, it is important to evaluate:

- Remaining policy tenure

- Guaranteed benefits

- Accumulated bonuses

- Tax implications

- Surrender value

- Alternative options such as making the policy paid-up or taking a policy loan

In many cases, consulting an experienced insurance advisor can help identify better alternatives than surrendering the policy.

Recent IRDAI Rule Changes Improve Surrender Values

The Insurance Regulatory and Development Authority of India (IRDAI) has recently introduced new surrender value regulations aimed at improving fairness for policyholders. These rules increase the amount payable when eligible traditional life insurance policies are surrendered after meeting the prescribed conditions.

While these changes provide better consumer protection, they should not be viewed as an encouragement to surrender policies. The primary objective of life insurance continues to be financial protection rather than short-term liquidity.

What Should You Do Before Surrendering Your Life Insurance?

Before making a final decision, ask yourself the following questions:

- Does my family still need financial protection?

- Can I reduce premium burden instead of surrendering?

- Would converting the policy into a paid-up policy be a better option?

- Can I take a policy loan instead of terminating the policy?

- Have I compared all available alternatives?

A policy surrendered today cannot usually be reinstated on the same terms later. Therefore, every decision should be made after carefully considering both immediate needs and long-term financial security.

The Bigger Lesson for Every Policyholder

The increasing number of policy surrenders reflects an important lesson—buying the right insurance policy is far more important than buying insurance simply for tax savings or investment returns.

Life insurance should be selected based on your family’s financial responsibilities, income replacement needs, outstanding loans, children’s education goals and long-term financial planning.

When insurance is purchased for the right purpose, policyholders are far less likely to regret the decision or surrender the policy midway.

iAdvisor’s Perspective

At iAdvisor, we believe that life insurance is first and foremost about protecting your family’s financial future.

If you are considering surrendering your existing life insurance policy, seek an independent review before making a final decision. A professional assessment may reveal better alternatives that preserve your insurance cover while helping you manage your financial situation.

Remember, the cost of losing life insurance protection can be much higher than the money received through an early surrender.

Is surrendering a life insurance policy a good idea?

It depends on your financial situation and the type of policy you own. In many cases, alternatives like making the policy paid-up or taking a policy loan may be more beneficial.

Will I get all my premiums back after surrendering?

No. Most life insurance policies pay only the surrender value, which is usually lower than the total premiums paid, especially during the initial years.

What is a paid-up policy?

A paid-up policy allows you to stop paying future premiums while retaining a reduced insurance cover and certain policy benefits, subject to policy terms.

Should I consult an advisor before surrendering?

Yes. An experienced insurance advisor can evaluate your policy, compare available alternatives and help you make a financially sound decision.